Nathan Walker

Research is currently underway on how COVID-19 effected the UK and Ireland water sectors. The unprecedented scale and impact of the COVID-19 pandemic required organizations to adapt all facets of their operations, and the water sector was no exception. There was particular difficult for the water sector since they had a shift in demand from business to residential and an increase in overall consumption due to the emphasis on washing and hygiene to combat the virus.

We wanted to analyse how resilient the sector has been across the UK and Ireland to evaluate how previous policy and regulation prepared them, and how they can prepare for any future obstructive events. To do this evaluation, data was collected and analysed for 18 indicators from 19 companies for the years 2018 to 2021. We incorporated a variety of metrics to measure the resilience of the water sector, including economic, environmental, and service based data. Initial rudimentary assessment has taken place by averaging the data for the 3 years leading up to the pandemic and comparing it to the first year of restrictions.

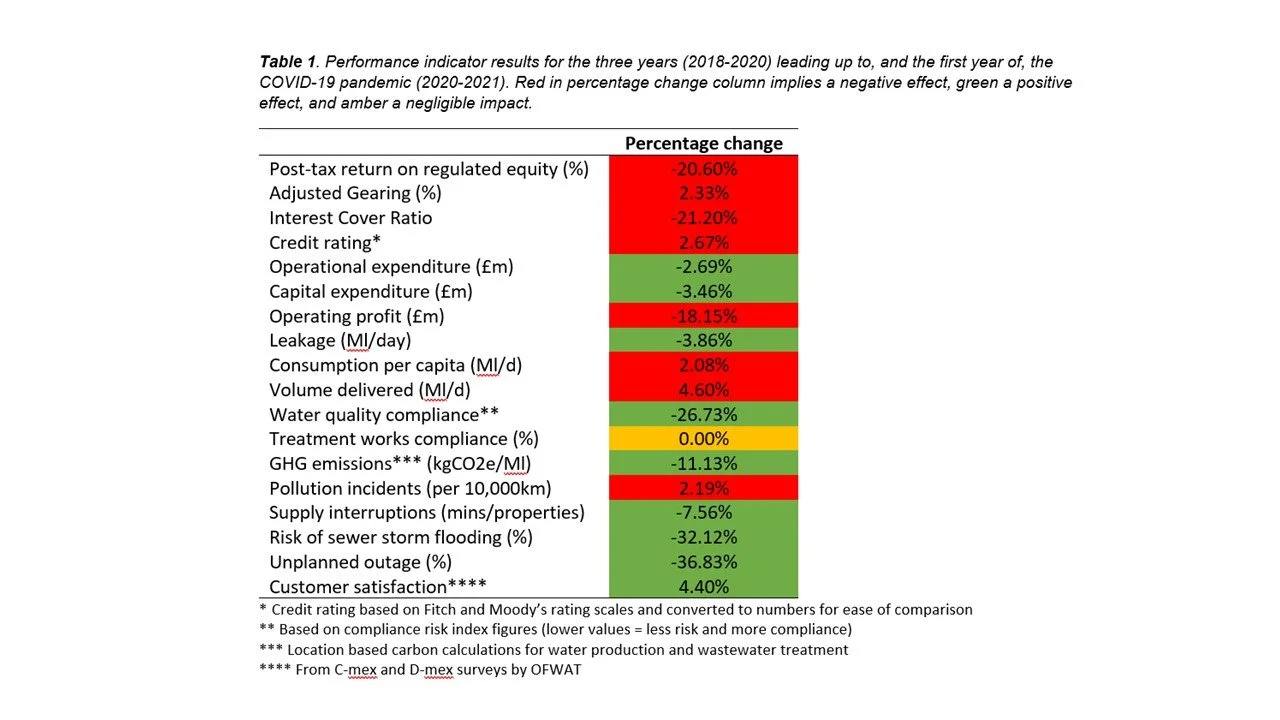

Initial results, presented in Table 1, suggest the water sector had a mixed response to the pandemic, where eight indicators are marked red, nine are green, and one is amber. This is nearly an even split of positive to poorer performance over 18 indicators, particularly since even the amber result of treatment works compliance was still performing at a high-level sector-wide despite the lack of change.

The largest positive changes were exhibited by unplanned outage, which reduced by 36.83%, this was closely followed by risk of sewer storm flooding with a decrease of 32.12%, and water quality compliance, which had its measurement of compliance risk reduce by 26.73%. These are significant reductions and improvements to the service and security of water to consumers, despite an increase in total and residential water demand. The significant improvement in water quality compliance could partly be attributed to the lack of residential sampling opportunities caused by government-imposed restrictions, although alternative sampling was sought from staff homes, commercial premises, company property, and when these options were unavailable, surrogate samples at service reservoirs. The most negatively affected aspects of the UK water sector were revealed by the indicators: interest cover ratio, which suffered the largest negative impact of -21.20%, followed by post-tax return on regulated equity with -20.60%, and operating profit with -18.15%. These results were likely the result of an increase in costs incurred by the rise in volume being delivered to households, health and safety costs, and increase of unpaid bills.

Work is currently being undertaken on diving deeper into some of these perceived performance changes, with a view to highlight specific excellence in resilience at the company-level. This research is under development and thus, results are subject to change.